Slowing cost growth and an increase of consumer-directed health plans linked to Health Savings Accounts, may be very early signs of healthcare consumers taking greater responsibility for, and control of their healthcare. It may also signal a dangerous shift in risk.

A recent national survey by the consultancy Mercer showed that a rate of growth in employer-sponsored health insurance premium costs was only 2.4% in 2016. This is one of the lowest rates in decades.

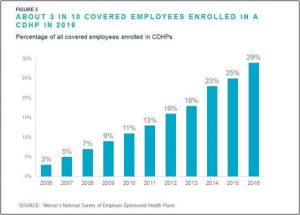

Part of the slowing of premiums cost is due to the shift to consumer directed health plans (CDHPs) linked to Health Savings Accounts, with an increase to 29% from 25% in 2015.

Risk and reward?

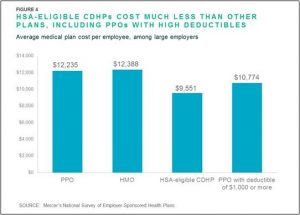

One of the most likely reasons for the growth in CDHPs is the difference in their cost. The survey pointed out that the average CDHP cost $9551 per year, whereas the HMO and PPO costs were $12,388 and $12,235 respectively.

A central feature of consumer driven plans is the shift of risk from the insurance carrier to the beneficiary. Basically, consumers are taking a risk that they can pay for needed or desired services out of premium savings deposited into the Health Savings Account (HSA). Beneficiaries who consume no or few medical services “win”, whereas those who have expensive services during the benefit year may find themselves exposed to significant liabilities.

Consumers take charge?

This exposure should motivate consumers to be more responsible, take better care of their health, and be smarter consumers of health care services. Unfortunately, consumers in the United States (and elsewhere in developed countries) have proven to be poor “customers” of healthcare services. The research has shown that, when people get sick, they don’t shop around, comparing performance or outcomes of providers to reach a decision. This “shopping” behavior would be considered the search for value, which consumers demonstrate in many ways in many markets. Instead, healthcare consumers choose local providers, or ones with which they are familiar, or providers recommended by other healthcare professionals such as physicians or nurses, or even friends.

Double whammy

It appears that beneficiaries of employer-sponsored health plans are taking on more risk, even though they lack the savvy to shop for value. This highlights the need for further developing healthcare consumer shopping behavior. Lower-cost, high quality providers may be able to lead this educational effort. Whether these high-value providers are local or at distance, or overseas, there appears to be an opportunity to help beneficiaries in employer-sponsored health plans to avoid the double whammy of higher risk exposure, and lack of shopping savvy.