Declining demand in long-term care markets is not a popular topic, but the inaugural SNF report from the National Investment Center for Seniors Housing & Care (NIC) clearly shows this trend. The occupancy rates in long-term care markets have been dropping, and in the SNF category, occupancy fell from just under 85% in October 2011 to 82.8% in December 2015, according to NIC. The decline in occupancy in this specific long-term care market would have been worse if owners and operators had not been removing capacity (taking beds off-line) from the system progressively over the same period of time. When both the number of beds is declining, and occupancy is decreasing, how can this be described as anything but a late mature, early declining market?

Declining demand – occupancy falls

The NIC report suggested that the decline in occupancy was due to lower lengths of stay in the short term care patient category. But these numbers don’t add up. In 2015, there were approximately 1,000,000 joint replacement surgeries, which represent the majority of short-term rehabilitation admissions, to SNF. And if (optimistically) 30% of these were admitted to SNFs for rehabilitation, and the average length of stay was 15 days, this market would be approximately 4.5 million patient days for SNFs. On the other hand, the decline from 85% to 82.8% represents 13.7 million patient days. There are clearly other forces at work here.

Demographics – like gravity

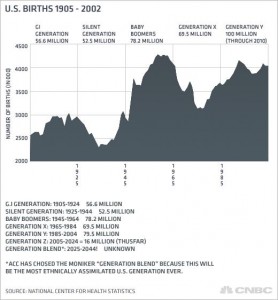

The biggest single factor in the decline in demand in the long-term care markets is the Demographic Dip or Birth Dearth. Demographics are like gravity; you can learn to work with it, but you can’t deny it.

From 1925 two 1945, the live birth rate in the United States (and elsewhere in the Western world) declined precipitously due to the Great Depression and World War II. With the average age of admissions to SNF at approximately 87, and the average age of relocation to an assisted living residence at 86 in 2015, these individuals were born just at the beginning of this decline in live birth rates. In other words, occupancies are down because the market (the number of age qualified individuals) is declining.

Volume to Value: A race to the bottom?

Compounding the challenges of declining long-term care markets, are the initiatives by CMS and other managed care organizations to reduce utilization, and “squeeze out” margin in the sector. The transition from volume-based payments to value-based payments through such mechanisms as Accountable Care Organizations (ACOs) and Bundled Payment for Care Improvement (BPCI) are laudable and needed, but these will have devastating effects on the sector. The shift from volume to value will benefit the strongest (i.e., SNFs with the best quality payor mix) and disproportionately hurt SNFs serving the most vulnerable populations in our society. As intermediaries and value-based payment initiatives reduce utilization, and margin from the sector, the weakest will be forced to either close or merge with other, bigger and stronger systems.

Lessons from other sectors

How should owners/operators respond? The decline in demand in the long-term care markets is not new, and lessons can be drawn from other sectors which have gone through similar business/market lifecycle changes. What’s impressive, however, is the organizational resistance by professional groups to admitting that the market is declining at all.

Best business practices from other stagnant and/or declining markets show that selected organizations can thrive by:

• Defend, protect, and fortify existing market share. This is best done by managing for loyalty rather than satisfaction.

• Increasing efficiency. Long-term care markets have not yet started serious adoption of existing models of improving service-based efficiencies, and for many providers, this is an existential urgency

• Innovate. Implementing real change in the products and services being offered is essential to both protecting market share and securing the future.

• Differentiate. If consumers and/or intermediaries can’t tell the difference between your Alzheimer’s or rehabilitation program, and your competitors’ – how are they going to choose?

Next steps for survival?

Without specific market analysis and evaluation, it is hard to say what the next steps are globally, but for some

providers, closure or mergers may be proactive to an eventual and unnecessarily painful end. For other providers, a four step program outlined above can make the difference between survival and closure.