Date: 17th June 2020

To watch the recording click here

Register to download the webinar presentation.

Transcript

Long Term Care After COVID19: The Road Ahead Updated.

June 17th 2020

Irving Stackpole

Thank you again for being here. I’m both humbled and overwhelmed by the response to these to these webinars. We are three months into this event roughly, and the road ahead for long term care in the United States and the UK, in Europe and elsewhere is still taking shape. I want to talk about the current situation, I’ll talk about things in both economic and operational and marketing terms. I’ll talk about the means of production, supply and demand. I’ll talk about the likely recovery models for the sector, for the markets, for long term care and why this time really is different, and we’ll talk also about effective responses.

I want to define a crisis, any unexpected event with adverse effects on your organization, customers, consumers, on your brand and the usual sorts of crisis that my firm and other strategic marketing communications firms have dealt with over the years in the sector, our deaths and injuries which do occur, untoward deaths, injuries to residents and staff on premises or in the line of duty, violence in or around the property that these things happen.

Closures are untoward events in a community. And how they are handled from a marketing communications point of view is important for the long-term perception of the provider among its employees as well as the brand. So, what’s different in this?

This particular crisis is the media frenzy that that’s been created is it’s also different because it is personal relevance in this particular crisis, personal relevance for a very broad array of the markets that with which we communicate because many of us have a relative or a dear friend located in a nursing center, a care home or an assisted living residence, some type of congregate care setting. Another reason this is different this time is that the entire sector is under siege, the labels that have been used care homes, nursing homes, nursing centers, rehab centers, these are being used in media, more frequent way than ever before and in a negative way.

The other reason this event, these this time is different is because of the latent guilt in many societies around the relocation of or by consumers, elderly individuals to care homes to nursing centers. It’s a in many cases, unspoken, unspoken rule that we should be taking care of our parents or grandparents ourselves. And when we don’t do that, as we probably cannot but do not, there’s latent guilt associated with that. And the recent media frenzy is stirring that up and creating issues.

We don’t know when the situation, when the coast will be clear, so to speak. For caregivers, the issue is to who wants to work in an environment like this? Who wants to work in an environment where, for all we know, the caregiver, I myself might be the vector of the disease? Who wants to work in an environment where I don’t have access to testing, where I don’t have access to personal protective equipment?

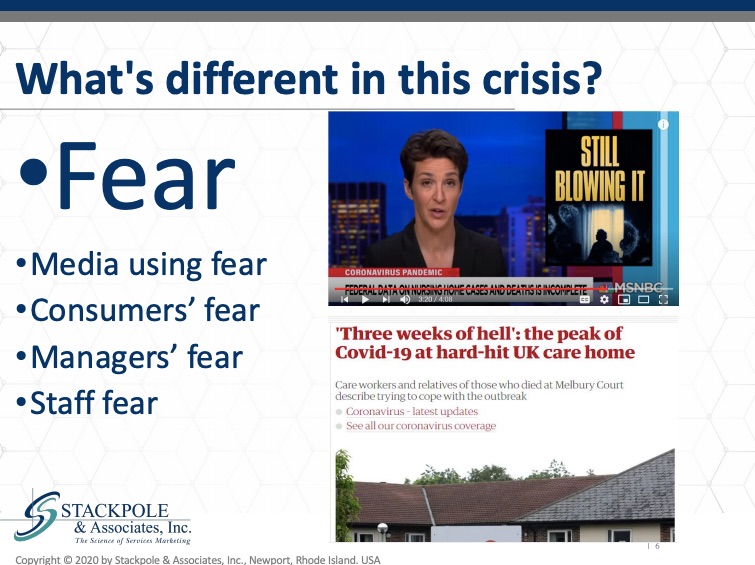

What’s different about this crisis? I think the dominant factor, is fear. Fear is a human and social experience; it is often described as an emotion. It’s been researched a little bit and surprisingly in this context, very little. And yet few things are more important right now because as we see here, Rachel Maddow and this other clip from The Guardian is using.

They’re using fear to sell their subscriptions to their outlets and newspapers. Consumers are frightened. Consumers are frightened overall about what do I do? What do I don’t do? What’s safe, what’s not safe? How do I behave in this heightened anxiety? This heightened uncertainty creates fear. That’s one of the things that we’ve been learning. heightened as well.

Operational managers, owners, operators are afraid because their business is under threat. So, in many cases, that fear is really quite legitimate. Staff are afraid. They’re afraid for themselves. They’re afraid for their jobs. They’re afraid for the people whom they’re caring for. We know from good research in the sector that staff develop very deep bonds, very deep relationships and effective relationships with the people they serve. And so if you’re uncertain about how you, as the staff member, might be negatively affecting the resident, that creates fear as well.

Let’s drill down into staff in the US and the UK.

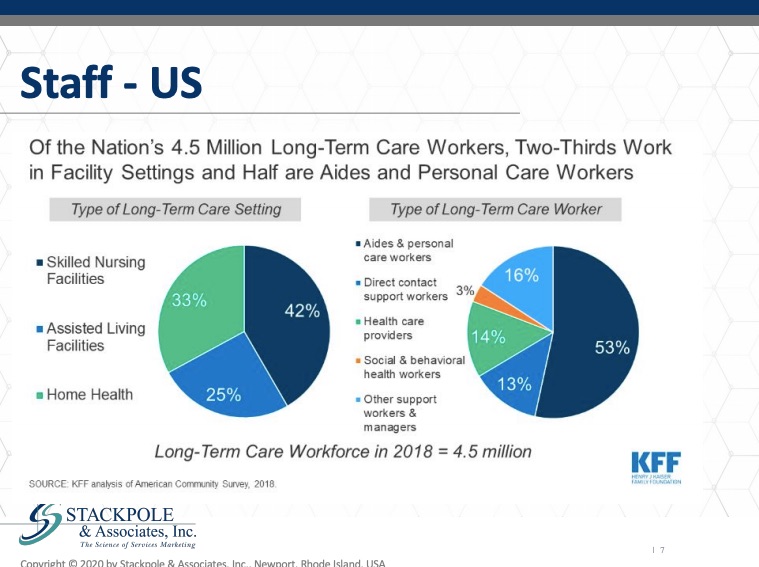

In the United States, there are about 4.5 million long term care workers. Predominantly they work in skilled nursing centers. Some work in assisted living and home health care as well. They are in the majority women. They are almost 25 percent of them are African American. That’s the case in both the US and the UK as well.

Where they fall on the social economic spectrum leaves them particularly vulnerable in this particular crisis in the U.K., that’s about 1.2 Million, about less than half a million work in care and nursing homes and about six hundred thousand in domiciliary care and one hundred and fifty thousand providing day and social care.

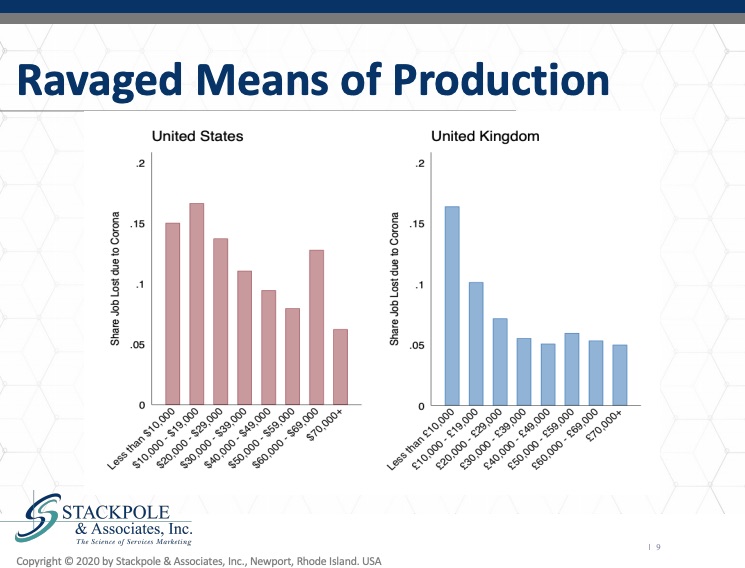

Now, this is a breakdown in the United States and the United Kingdom of the size or proportion of the individuals in these ages, in the income cohorts and who’s going to lose their jobs.

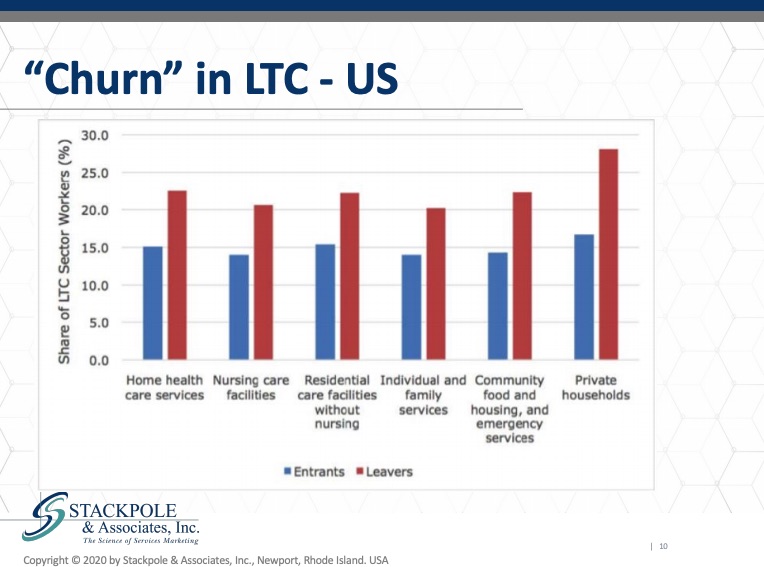

As we see it is the lower income groups who will share the predominant burden of job loss as a result of coronavirus. I want to drive this point home. These individuals who in a in an econometric point of view are our means of production. They are the ones who are actually doing the work. They are most at risk for losing their jobs. Their friends and family members are losing their jobs and they are at risk as well. This heightens the sense of fear and anxiety that our staff experience, while they are caring for the most vulnerable in our population in the US, we can see these numbers, which is reflects churn in long term care in the US. I’ve written about this extensively. It’s extraordinarily expensive. It is indeed a strategic vulnerability that in the US there is such a heavy level of turnover in the front-line caregiving categories.

We see this data here.

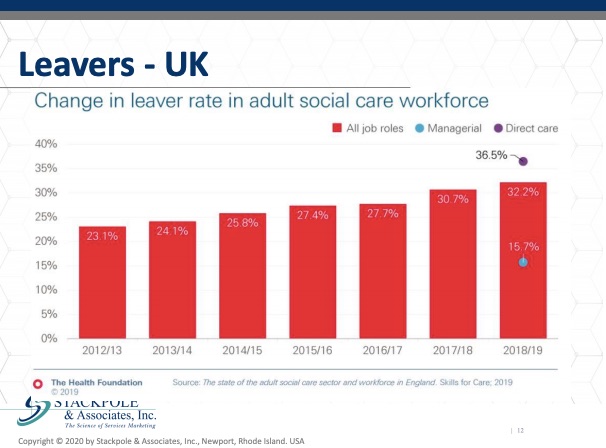

Similarly, in the UK, we don’t have the entrance data, but the leavers, the leaver rate in adult social care is extremely high.

We can see that in this source, which is from the Health Foundation, they anticipated in 2019 at 36.5 Percent, 40 percent of the frontline caregivers would be leaving their jobs. That’s it creates an extraordinary situation for operators. Here’s the situation assessment for the staff in long term care, the recruitment issues are challenging. Retaining individuals once we’ve recruited them is also a struggle when unemployment surges, as it is in most places around the world. The question becomes, will long term care be seen as a good alternative? One can say, well, if the local service lets the local hospitality, for example, hotels, if the hotel sector loses staff, there’s high unemployment, well, that bodes well for long term care. Well, does it? I would raise that as a question whether long term care will be seen as a good alternative as the economies open back up. It raises the question, who wants to work for you and how do we communicate?

We’re going to talk in the last section about how what we say and how we word our messages to our audiences is so critical at this time with regards to the supply, our physical property, plant and equipment, PPE, personal protective equipment, but in an accountancy or econometric sense, property, plant and equipment.

Our supply, our inventory, our capacity has been struggling. There’s been struggles with occupancy and that’s certainly occurring now. The most recent data about occupancy shows that the level of beds occupied in both the US and the UK and in other locations as well is declining. We’re struggling with recruitment and retention, as we’ve already talked about and importantly, the economic model is a struggle in only a few places in developed economies. Is there a sound economic model to pay for care in congregate settings?

The inventory is old and, in many cases, threadbare and unattractive. There is by any stretch an onerous regulatory burden in many locations for congregate care. There’s unfortunately a deeply negative cultural bias toward congregate, elderly, qualified, care. For years, my firm did a very large-scale survey for what was then Lifeline. It’s now Philips and we did tens of thousands of surveys of referral sources in the United States, in the UK and found that referral sources themselves consider relocation to congregate care an extraordinarily negative event.

So, in assisted living, that’s market rate, more voluntary and less need driven relocation. Occupancy is not as bad as it is in nursing centers and care homes. It’s balanced or struggling based on increased supply. Recruitment and retention are less of an issue. The economic model is better because there’s better margins and there’s an opportunity to create market rate charges because relatively low inventory. Its the buildings and the properties are more attractive is a minimal regulatory burden and there’s only a slightly negative cultural bias. And this see why that is in a moment. For independent, aged, qualified, independent living by age qualified congregate care centers, occupancy is in some locations quite good in other locations that’s been struggling with recruitment.

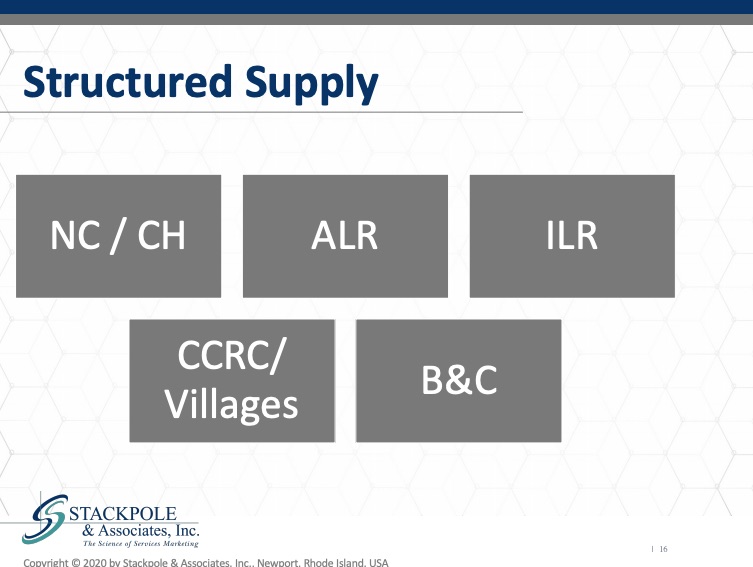

Retention is less of a burden because there’s fewer carer’s. Your caregivers needed to attend to the needs of the individuals who are resident there. The economic model is better, relatively new inventory, little and no regulatory burden and only a slightly negative cultural bias. Much of that cultural bias has to do with how the property is labeled or what it’s named. We typically in the management side of the supply system in congregate care, we typically structure the supply, something like this,

where nursing centers and care homes are in one bucket, assisted living residences are in another bucket, independent living CCRC or care villages. And this bright lines between and among these sometimes driven by the regulations sometimes. Driven by simply what the intention of the developer is, however, consumers see these all overlapping and that’s important as we look at how the sector might recover, how the sector will emerge as the economies emerge as well.

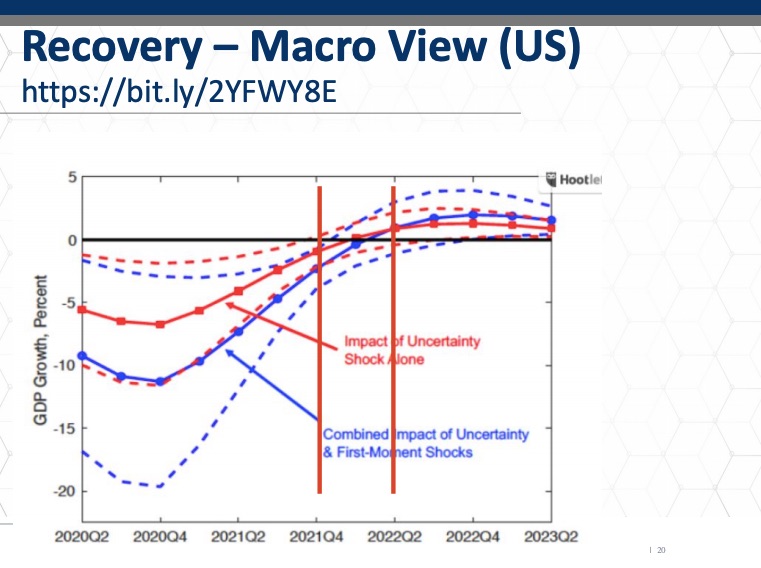

Let’s look at recovery with painted the picture of what the situation is. This is a model that shows the economic models for recovery based and based on the US.

This is a macroeconomic view of potential recovery models based on the supply and demand side shocks that the pandemic represents. What it looks like here is that the earliest time when we’ll see a return, approximate return to normalcy will be in the fourth quarter of 2021. Then this model shows that the normalcy begins to return in the second quarter of 2022. Now that may seem like a long way away given the scale of what has occurred. This despite the political positioning to the contrary. This might be a very reliable prediction of this economic event in many articles about the economic impact of the Covid19 sars-cov-2 pandemic. In many of these articles you’ll hear about you shape and v shake recoveries. This model shows a modified U shape, and you can see in the curve, the depression associated with the uncertainty, shock and the first moment shocks.

We are going to look a little more closely at this because I want to create an analogy between how the economy will recover and how the sector will recover, as I believe there is a legitimate analogy there to be made.

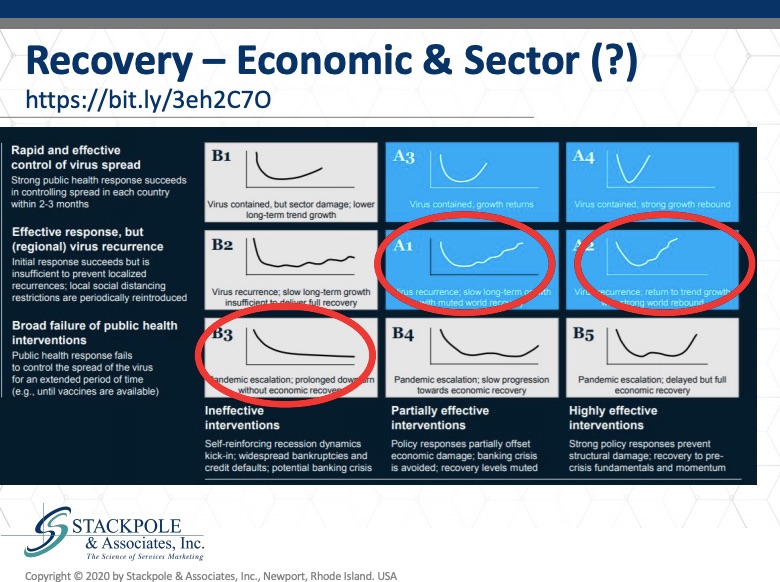

This is from McKinsey Report and it applies, I believe, to the economy at large and to the sector in particular. I want to point out here the center of these six potential economic recovery models. I want to look specifically at a one. It shows a long term slowly returning to normal, where we’ll see partially effective interim interventions and effective response by the public health authorities to the to the virus. But with recurrence, which is already what we’re seeing, we’re seeing recurrence around the United States, around the UK, but not in the densely populated epicenters that we had seen initially. Another slightly more optimistic perspective, which may very well occur, is in a tube where we see a recovery, a U shaped with an irregular recovery, but a more rapid recovery.

I’ve modeled some of these recoveries, which I will show you in a moment. Then the sort of the negative nobody wants to see this happen is what’s referred to as an L. Shaped recovery, where there’s a permanent where there’s permanent damage to the economy and a permanent loss. I think unless there is some change in the approach to Covid19 in nursing centers in particular, and care home care homes in particular in the US and the UK recovery. I fear that we may see permanent loss of market demand in those categories based on some inappropriate responses by the regulators and the public.

Let’s look at some of these factors in the post Covid19 time frame. The first of these is acceptance and the flip side of that, the obverse is penetration. So, if I accept congregate long-term care as a solution for my needs, I am part of a segment of the population. Not everyone for whom congregate care is a suitable alternative. Not everyone accepts it as an alternative, as a solution, so that this degree of penetration and acceptance, which we routinely measure in market-based feasibility analysis or market analysis, this is a critical factor because as many as the age, income, asset or disability qualified individuals there may be in a geography, only a certain proportion of them will accept congregate care as a solution. Then there are the tradeoffs between and among the needs or benefits and the risks. And that’s what Covid19 is doing. It’s introducing a new level of risk, which we must evaluate in the context of market analysis. And then the other bullet here is the tradeoff between the needs that I have or the benefits I perceive and the status quo.

Determining the level of acceptance against staying in your own home or staying in a relative’s home or staying in your current domestic setting. That’s always a difficult barrier to overcome. My concern is that going forward, that will remain a difficult barrier and become an even greater barrier to acceptance. Another piece here that’s very worrisome is government or regulatory intervention. How will that play out? Will it be supportive, or will it be punitive?

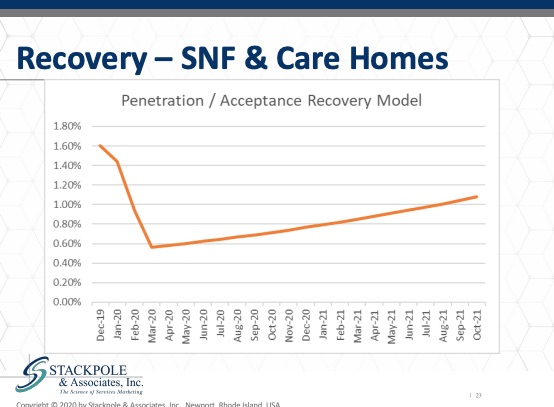

Another variable here that needs to be considered and this needs to be considered by the regulatory authorities and by government, is the liability issues and exposure associated with Covid19. Do we need special riders on our insurance policies? Will we need to have residents sign waivers? Will they accept those waivers? How will this be resolved? The insurance market has been silent so far, although I know that they are all there’s a lot of actuarial midnight oil being burned right now as we speak about that. What I’d like to do is offer what I think it’s just an estimate, a preliminary estimate of the timeline and the depth of and the scope of the impact of Covid19 on skilled nursing centers and care homes.

I’ve estimated using some rough national estimates, the level of penetration and acceptance for these solutions, and my concern is that the acceptance and penetration will indeed be plunged into roughly half of its current level and that it will recover only very slowly.

I believe that we will see a loss of further supply. Colleagues doing research in this domain have shown that in the United States we’re losing nursing homes. Nursing homes have been closing at a very rapid rate in response to demographics and payments, and that the loss of those nursing centers is primarily in less densely populated areas. In places, it’s things like places where they’re needed the most, they are going away the fastest. And I am concerned that the same pattern will manifest in the UK and in the EU as well in market rate assisted living.

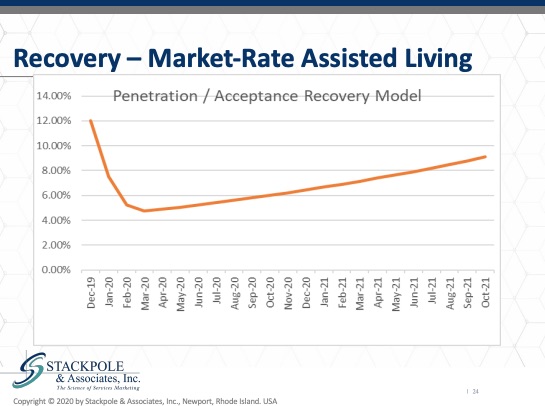

As you can see, the depth of the acceptance will be less, the trough will be lower and the recovery swifter. But it still remains to be seen how negatively certain assisted living residences will be viewed by the consumers. A lot of this will be determined by the nature of the acceptance in the marketplace area before Covid19 and in places where the acceptance rate was previously very high. We believe that the virus factor, the negative effect of Covid19 will be attenuated by that high level of acceptance in marketplace areas where acceptance was low. We anticipate that the depth of the losses in market acceptance will be higher. And for independent living, we see also see a loss, a significant loss of acceptance and penetration, but a swifter return also depending contingent on branding and the how badly the virus was, how badly the virus impacted in the local marketplace area, and how much negative press the skilled nursing care homes received in that local marketplace area.

I’d like to now go through a couple of models that are possible, in my estimation, for recovery in the sector and the economic depth, length and shape in the marketplace area will certainly impact the effect on the sector. I think basically two potential scenarios. Scenario one is that the sector will have a bonafede opportunity to rebuild and recharge, and that’s going to rely on policy, that’s going to rely on politics, that’s going to rely on sane voices coming forward and saying we simply cannot tolerate an irrational, completely inefficient from an economic point of view, from a human point of view, it’s a completely inefficient system and it needs to be rebuilt and recharged.

The other potential scenario, unfortunately, is ravaged and relegated, ravaged based on occupancy and the financial turnover that these operators may have and relegated to further second-class status, which is where, unfortunately, nursing homes and care homes are currently. So those are the potential outcomes and the outcomes in terms of recovery for economies and the sector. And I believe that they will be very closely related in most places.

What we as operators, managers, some academics do. What are some of the effective responses? This is built on extremely good, extremely sound research on effective communications in a crisis and how our communications can impact either heightening or lowering the reactions to situations that are present in.

The first thing we can do is have a crisis communication plan. The first crisis communications webinar was a month ago. And as I told you then it’s even more important now because a plan includes how we manage the media as well as how we manage the messages. We have to take responsibility for the messages. That means not waiting for media or special interest groups in the U.K. We can’t wait for skills, for care. We can’t wait for advocacy groups to take up our cause for us. We need to take responsibility for that. And in the United States, leading Asia’s step forward and get a pretty good job of advocating.

But we operators and managers, we need to take responsibility at a local level to manage the impact of this crisis in our markets. The second thing is that we need to be scientific and numeric versus affective. What the good research shows is that our messages need to focus on numbers. We need to focus on the science and not on the emotional side of this of the of the messages. There are certainly some positive stories. We talk about health care heroes. That’s effective and a very positive story. I have clients that have congregate care centers on islands and those situations are quite favorable. That’s a good story. But the principle here is that the communications should be scientifically based, and it should be numerically based. Shaming, which is I don’t have to explain shaming, shaming, it’s being used certainly in the Twitter sphere, in the digital communications by many people around the problems in long term care and care homes in the UK and nursing centers in the United States. The other principle is that we need to shift the narrative now. We need to start telling the stories that are scientific numeric but talk about the positive aspects and there are some positive aspects. We need to tell those stories and show those images. Now, we need to begin to develop this capability and this trickle of communications into our local marketplace areas. The second thing that we absolutely need to do is we need to review our digital assets.

We need to have crisis communications that accept and understand the principles of perceived risk, is having an impact on fear. And we can mitigate that. We can reduce the impact of perceived risk by talking about our centers, our experience, what we were able to do successfully, numerically and scientifically, and that will reduce levels of fear. And the other is we’ve never really done a good job of this in our in our businesses on either side of the pond.

There are certain segments of our populations, of our target populations who will be more amenable to a congregate care solution than others. And we need to be smarter and more efficient about reaching out to those segments for nursing centers and care home care homes in the UK, consumers and staff. These segmentations can be undertaken very specifically with regards to recruitment and retention. Why do people keep working for us? There are people in our centers who have been extraordinarily loyal, who are deeply committed. Let’s better understand who they are and why they’re motivated to undertake these extraordinary measures. Let’s understand that better and then use that information to better target, recruit and retain individuals. The other principal, the last principle in this set of here’s what we can do today, we can protect, defend and fortify our current market share. We can protect, defend and fortify our current staff, which I’m sure many of you are doing the. Principle here is service error recovery, we’ve had lots of errors now we need to implement effective service error recovery. And for those of you who participate in other participate in other trainings that have presented, this is worthy of its own topic. It’s critical there is a science behind how to recover from an error that one commits in a service environment, and we need to get smarter about that in long term care.

Finally, we need to innovate for greater efficiency. If the markets are going to shrink and the available means of production are going to be more difficult to find, we need to get more efficient. I believe efficiency, real efficiency will become an extraordinarily important hallmark of successful providers going forward. Finally, we need to differentiate it to differentiate around that higher level of efficiency and innovative, innovative ways to care for the people entrusted to us. In conclusion, we’ve looked at the current situation. We’ve looked at likely recovery models for both the economy and how that will be analogized to the sectors. We’ve looked at what managers can do today to help manage and accelerate effective response to Covid19. My hope is that these things have been communicated effectively and that there’s some insights to be gained as a result of this. And now I’d like to consider how I can answer your questions.

Questions

Question: Could you mention again the source of this recovery module?

Yes, the six-position grid was developed by McKinsey and it’s focused on the US. The other model that I shared with you is based on the UNWTO, the UN World Trade Organization’s estimates of global economic recovery. I use two models, one to show an international perspective and the other to show a more US based perspective. But these models, as I’ve looked at them, being shared in various articles and research journals, they appear to be quite consistent. There was a there was a 2006 study done by the EU, sponsored by the EU that anticipated a pandemic and what the global response would be to a pandemic event. And these academic researchers concluded that the recovery would be a V shaped recovery and a V shaped recovery is just as you can imagine it, a swift plunge in domestic production or a swift plunge in output, and then a swift ascent of output back to the same level. And that was basically their prediction, based primarily on how they viewed the events in 2008, 2009, the previous global recession. However, I don’t believe that that’s going to be, and many people are now in agreement that it’s not going to occur like that, that the global recession was a supply side shock and that this recession, which we’re certainly in now, is both supply and demand side shocks. And we simply haven’t had seen anything like this before. The closest analogy, of course, is the two thousand, the 1917-1918 Spanish flu epidemic. And that recovery was indeed, as I modeled for you. This more of a not even really you, but sort of a Nike swoosh.

Question: We agree that the infrastructure and especially the financing of the home sector is crippling the care of frail older people. But we but we do need some better version of CAMHS. Dispersing the cash to where people live in their own homes is not a viable alternative, but simply create thousands of institutions of one where older people are isolated out of sight and open to neglect. What steps must we take to maximize the good care to be found and the present facilities in a new model?

But a terrific question, first of all, I agree with the point made in the preamble to the question that domiciliary care or home care doesn’t address the fundamental issue of loneliness, social isolation. There’s very good evidence that isolation contributes to deterioration in overall health and it needs to be included in any social determinants of health. It’s a public health challenge of the first order. With that being said, there are some individuals who don’t do what’s necessarily the right thing for themselves and accept a solution that might be better for them, they prefer to be cared for in their homes. And when an individual insists on that, as long as they’re safe and not in any danger to themselves or to others. Systems should be available to deliver that. The problem is that in a in a viral pandemic, the individuals going into the consumer’s home are potential vectors for the virus and there’s simply no way to surveil and to protect that those vectors to assure that those vectors will be virus free and to surveil the consumers.

This is a situation where quite opposite to what may seem to be common sense in a pandemic is if the policies are in place. And I in many places they are and have been, it’s safer to put vulnerable individuals in a single place where you can monitor and control those who come in and the materials that are used to care for them. With that being said, I think what the questioner was really asking is how do we create a viable, sustainable congregate, long term care capacity, a supply capacity in the UK in particular, and in the US? Well. In many ways in the U.K., the challenge is scale and replicability. The second challenge in the U.K. is the financing mechanism. The financing mechanism, without getting into details in the U.K., is intermediated by local councils. It’s intermediated in a way that prevents a broad scale improvement of the efficiency of the way the money is spent. This has been highly politicized, and I would say historically somewhat frivolous ways.

First of all, from a money point of view, that needs to be addressed. Second of all, I think the UK is better off than the US in some regards in that the units, the individual care units are smaller than they are in the United States. The average size of a nursing center in the United States is over one hundred beds or units. The average size of an assisted living residence in the United States is over 70 units. The average size in the UK is much smaller, which allows for should allow for greater levels of flexibility. So, what we need is we need a policy discussion informed by finances and a reevaluation of supply and demand, it’s clear that there are millions of people in the UK and the EU, millions of people in the United States who need, want and would benefit from congregate care. We don’t have a system in either location right now that’s in any way rational or in any way efficient in order to do that, in order to really not waste this crisis, we need public voices, private voices pushing forward to create the discussion about how to better finance, how to better deploy, how to better build these care centers for the future.

Question: I find it very disturbing; the news media always focuses on negative issues and yes, there are some bad situations, but the largest majority of facilities and staff are giving their heart and soul to take the best care of their residents, sorry, in a very difficult and challenging environment.

Well, I have the turn that I have to turn that comment around, as I typically do in these conversations. I’ve been I’ve been involved in this sector since 1985. I came out of the general admitting hospitals in the United States and internationally, and I began working in the long-term care sector in the United States in 85’ and started working in the U.K. in 91’. I will hold up the mirror to you, to that person who made that statement and say, why aren’t you promoting the stories that you want to have promoting. You have access to the media and the media can be used as a tool far more effectively.

We can’t wait for the media to come to us and say, oh, if you’ve got a good story for me, no, we need to take charge now and be responsible for the messages that we’re delivering, managing long term care environments, whether it’s home care, or any type of long-term care environment is extremely complicated, in part because of the regulatory burden that’s been layered on top. So, the managers in these environments have had to be extraordinarily attuned to understanding these layers. It’s also been challenging to recruit and retain frontline employees and employees at large. The managers have been focused on those two topics and I’m sorry to keep in yet a third one on to you, but this is the time to take charge of the messages that we’re delivering into our marketplaces to our consumers. These messages need to be clear and positive. They need to be focused on numbers, not proportions, not percentages, but numbers. They need to focus on the science. We need to find a way to spin the message positively.

Resources

- COVID-19 and Workers at Risk: Examining the Long-Term Care Workforce

See: https://www.kff.org/report-section/covid-19-and-workers-at-risk-examining-the-long-term-care-workforce-tables/

- Analysis by the King’s Fund suggests the NHS workforce gap could reach almost 250,000 by 2030

See: https://www.kingsfund.org.uk/publications/health-care-workforce-england

- The Elephant in the Room: Staff Turnover 2017

See: https://www.relias.com/blog/staff-turnover-in-long-term-care

- The Health Foundation

See: https://www.health.org.uk/publications/long-reads/health-and-social-care-workforce - US model of GDP

See: https://mrzepczynski.blogspot.com/2020/04/uncertainty-and-covid-19-recession-it.html - This matrix from McKinsey shows the possible economic recoveries based on two factors

See: https://www.businessinsider.com/economic-outlook-9-scenarios-coronavirus-recovery-recession-mckinsey-experts-2020-4

Stackpole & Associates is a marketing, research & strategy consulting firm focused on healthcare and seniors’ services markets. Irving can be reached directly at istackpole@stackpoleassociates.com.