Date: 20th May 2020

To watch the recording click here

Register to download the webinar presentation.

Transcript

Long Term Care After COVID-19: The Road Ahead

May 20th, 2020

Irving Stackpole

It’s a pleasure to see you all here. I’m both flattered and humbled by the participation in this event and in the prior event, the Crisis Communications webinar that was done last week. I am excited because there’s such a high degree of interest and humbled because while I’m going to be sharing my experience with you, the topic is very large, very broad, and that the anticipated changes, the road ahead is still evolving, it’s still quite complex. What we hope to review today is the current situation where we are, and I’ll be talking specifically about segments in the markets for congregate long-term care.

I’ll be talking about likely recovery models with a couple of scenarios for that and then also talk about effective responses and what it is that we in the congregate long term care sectors can do.

The current situation, the easiest way to describe it is that we are certainly in a crisis. The words and hyperbole used in the media about the pandemic. The coronavirus pandemic but is indeed an unexpected event which is having serious impact on our customers, our consumers, our employees and the brand of congregate long-term care. A significant portion of what I’ll be discussing in terms of the road ahead involves managing your brand, managing how the public sees you.

The question is, what is our brand here?

I think these are National Guardsmen outside of a skilled nursing center being decontaminated after going in to be of assistance and helping. This is this is not exactly how any nursing center or any assisted living residence, any congregate care center, wanted to have its brand represented. The typical defenses, particular responses in the past that I’ve heard from clients discuss when discussing crisis communications and crisis management is it’ll never happen here. Families love us. Our referral sources love us. We know how to handle this, and my team can take care of it.

Well, what’s different in this situation is that Grandma, the consumers we care for who are placed in our trust and who’s the confidence of the families that we take on grandma is threatened. The second thing is that the entire sector is under siege and it’s under siege from many, many different angles, angles that we don’t necessarily have control over or can manage.

The problems I believe is significant latent guilt in our culture about not caring for grandmother at home. Now, I know that this isn’t with everybody. I know that not everybody feels this guilt. But there is a legacy, cultural bias to for those who care for their parents at home. That is, after all, an important feature of a culture that a culture cares for its elderly. And when we’re, for whatever reason, unable to care for our parents are elderly family members in our homes and need to seek care in a congregate care facility. There’s very often guilt that stirred up and that is getting an extra turbo boost in this environment.

Another factor is that there’s just no certain end to the challenges being presented by the pandemic, by the political and the systemic difficulties that we have having in addressing the crisis and the one of the biggest challenges that we’ll zero in on its staff. In a typical econometric model, the staff in a congregate care center, a nursing home or an assisted living residence, the staff are what makes the service possible. So, economists would say that your staff are your means of production. It’s how you do what you do. Well, in this environment, the means of production are also under threat. And that raises questions not just now as staff are decimated by this illness themselves, but also what impact that will have on recruitment and retention in the future.

Looking quickly at the staff in nursing centers across the United States. This is recent data from the Kaiser Family Foundation.

The four and a half million people who work in long term care centers are primarily working in skilled nursing centers, about a third work in home health and about a quarter work in assisted living residences. And they are overwhelmingly women and they are asked they are asset constrained, income, limited and employed. They are working paycheck to paycheck, and they are impacted by what’s occurring in our building significantly.

Let’s go on and do a further situation assessment in three product categories: skilled nursing, assisted living and in independent living or market rate age qualified congregate housing, well skilled nursing. The situation just up to the period when Covid19 came upon us was that skilled nursing was experiencing struggling occupancy. Occupancy had been declining. Depending on whose numbers you look at, national data suggested that occupancy in nursing homes and skilled nursing centers was somewhere around 80 percent. I believe that’s actually lower in the individual market studies.

Stackpole & Associates has done marketplace to marketplace research and often see skilled nursing occupancies at or below 70 percent. I believe that the national average is a function of rounding from both the statistical market areas where occupancy is very good, and those rural suburban exurban nursing centers where occupancy is very poor. Also, the major source of occupancy estimates in this category is primarily through the NEC data and the data is a sampling from it’s the largest available sample. It’s a good sample, but it’s predominantly from the very high end, well off nursing centers, which may present some bias in the reporting they are nursing centers that we’re having difficulty with recruitment and retention.

This is an issue with payment model. 65 percent of the population in nursing centers are Medicaid beneficiaries, and Medicaid is notoriously the low-cost reimbursement. That gets to the economic model, which is struggling. 65 percent of the population is being served at a loss and 10 percent of the population, the Medicare Advantage and private pay are cross subsidizing the Medicaid population. This is a legacy problem. I’ve written about it extensively. Skilled nursing centers, fundamentally old inventory. Virtually every state has a condition of need, certificate of need, requirement for new construction. And there’s been very little new construction in skilled nursing across the United States. Most of it’s been replacement. There’s onerous regulatory burden.

A colleague of mine who with whom I was talking earlier today said that just in the past six weeks that between OSHA and CDC. Seventy-seven hundred and sixty-eight pages of new guidance have been issued. This is a classic onerous regulatory burden. Finally, there’s a deep negative cultural bias toward skilled nursing. Nursing homes are not held in high regard. They’re not viewed as a as the critical solution that they are in the communities they serve very often. They are seen as places of last resort and seen and not a positive light at all, which makes the current environment all the more difficult. The in addition, in assisted living, the I just want to mention with regards to nursing homes, the issue with nursing homes going back to the nursing home piece, the issue has been this market mix of residents often referred to as quality mix. What that really is code for is the proportion of the residents in a particular nursing center that are being paid for through Medicare, Medicaid or through Medicare Advantage or through private pay. That’s the quality mix. And what that means is those are the patients on which the nursing center, the positive margin and that positive margin needs to cross subsidize the negative margin associated with the Medicaid beneficiaries.

In assisted living, the occupancy situation has been a little better. The occupancy overall has been relatively stable. It’s been probably impacted in certain marketplace areas in certain standardized metropolitan statistical areas by additional supply. Eager developers, eager builders, cheap money has been flowing into assisted living and developing assisted living properties in marketplaces with anything like good occupancy rates in an attempt to grab some of that occupancy. So that has stilted the occupancy rates.

Recruitment and retention is also a challenge within assisted living, but it’s a little easier, easier than it is in the skilled nursing environment, in part because of the social model and the programing that’s available in assisted living and also because of the lower regulatory burden within assisted living and frankly, assisted living, because the newer inventory generally more attractive places to work, the physical environment is better. So, the newer inventory, lower regulatory burden, and there is still nevertheless a somewhat negative cultural bias toward assisted living in the inmost marketplace areas. Look at why in the age qualified independent living markets, the so-called independent living independent living is a label that it’s also applied to another category in Health and Human Services, which makes it a little different. But in our lexicon, we talk about age qualified congregate market rate properties as independent living residences.

They’ve been experiencing flat or declining occupancy. Recruitment and retention is not a burden in this environment because the staffing ratio, the staffing is very, very light that the economic model is a simple rent or lease model. The numbers are easier to understand. And generally, the inventory is newer. There’s little or no regulatory burden and there is a slight negative bias, but less so than in comparison to skilled nursing and assisted living.

We typically inside the sector, talk about structured supply, looking at the skilled nursing SNF, skilled nursing facilities, assisted living residences, independent living residences, and then continuing care retirement communities.

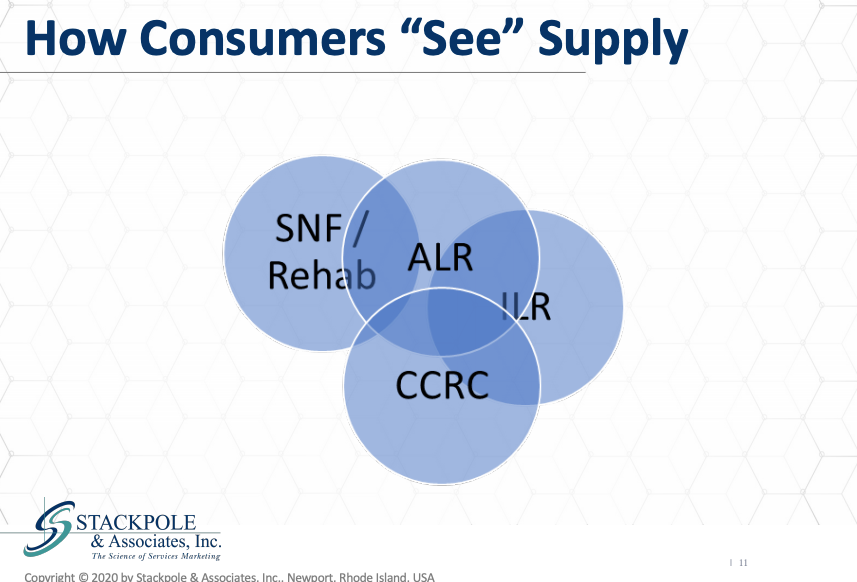

And the B and C there refers to a board and care home. This is the way that we look at the structure of the supply in congregate H qualified housing. Now, that’s not how consumers see the supply. Consumers conflate all of these categories and see many of them as overlapping, and they generally have a very difficult job discriminating between and among the categories. This has been very evident in many, many surveys that Stackpole & Associates and other colleagues have performed in the markets, in the United States and in the U.K., suggesting that the sector, the congregate long term care sector has done a very good job at all at differentiating its product for these markets.

So the consumer market sees supply as this overlapping Venn diagram of product, and that’s relevant for the road ahead, inasmuch as a negative perception in one of those overlapping circles is likely to impact on and affect another of those circles, they are indeed conflated in the minds of consumers and how they see skilled nursing, how they see nursing homes also impact, how those same consumers see assisted living and to some degree, continuing care, retirement communities and even independent living. So that’s the situation that’s the place we were we are at with congregate, care, congregate age, qualified care in the United States and this these factors will all play a very important role in the road ahead, because what we’re interested in is how are we going to recover the situation in most congregate long term care centers is has been very bad for the past several weeks. Tragic in some in some ways.

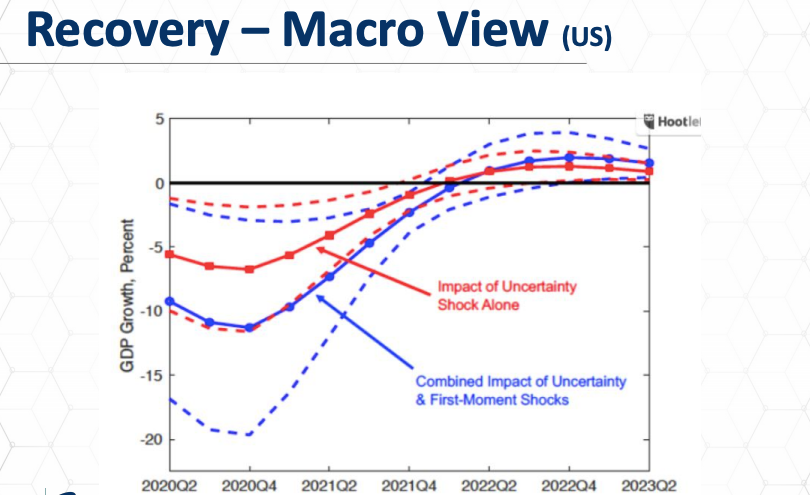

So what is the road ahead? How can we anticipate or predict? And importantly, what do these models for recovery show us how to behave now? What can we do today that will make the road ahead better, smoother, have and do a better job of assuring our survival into the time ahead? Well, in a macro view, this is a way of looking at recovery. This is an economic model. I believe this is from the United Nations about the United States and the impact of the Covid19 on GDP growth and how this will play out over time.

So you can see here that there are various ranges of effects based on certain variables, uncertainty about how the country will deal with the public health issues, how effectively those medicines will be, how effectively mitigation or suppression effects will be, and understanding that this is still an evolving situation. Most of these models show that by Q4 in 2021, there is some level of recovery that’s occurring in GDP and other economic indicators. This is important because we know from the 2008 2009 Great Recession that the reduction in employment and loss in GDP growth had both had a significant impact on the consumption of health care. Health care consumption went down as a direct result of the 1928-1929 Great Recession. But also, there were significant impacts on the rate of acceptance, the absorption of assisted living market rate products, as well as in nursing home occupancy as well, directly related to the recession, the Great Recession.

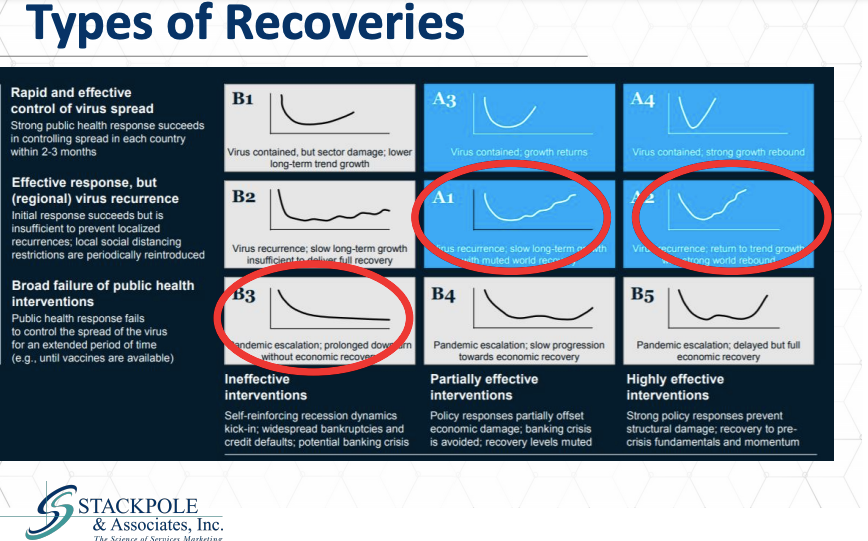

We are entering a period of economic recession, possibly depression that’s even greater than that. We can anticipate these effects. McKinsey put together a very nice set of models. I’m quite confident that within congregate long-term care, we’re going to see a few different types of recoveries.

I want to point to this model, a one in the McKinsey model that shows a steep drop in economic activity and then a slow hesitating emergence from that drop back toward stability or back toward point A, where we started, I believe, overall for the congregate long term care sector in balance. That’s the type of recovery we’re going to see with some slight modifications and exceptions, which I am going to delve into a little bit.

Another possibility, and I believe that this is likely for the independent living market, I think we’ll see a swift return, a more abrupt upturn in demand as the markets emerge, as individuals feel slightly more secure. There is latent demand that’s building up during this hiatus, during this period of lockdown, quarantine, epidemics, depression, pandemic isolation, during this period, this pent-up demand. The market model that appears in the three year in the McKinsey model shows what’s referred to as an L. Shaped recovery, and I believe that in skilled nursing, that’s the risk. The risk in skilled nursing is that the loss of referrals, the loss of new client’s deaths and the departure of existing residents, for whatever reason will not. That will be enduring that that change will be lasting. Again, this is going to be varied from location to location. If you put together the factors here that will impact the road ahead for congregate, seniors housing, congregate age, qualified housing, the first of these factors is acceptance.

The other term is penetration. Penetration is often referred to in feasibility studies as the number of or the proportion of age, income, asset and otherwise qualified individuals who actually choose a particular option.

So, if in a particular marketplace area like Boston or Atlanta or Orlando, you have a certain number of age qualified individuals and then smaller than that group is a number of income or asset qualified individuals of that group of age, income and asset qualified individuals, what proportion of those people actually accept congregate seniors housing as a solution to them? Now there’s variables involved. There are psychographic variables that disability variables and each of those needs to be looked at carefully and every individual market study but study. But very broadly, the rate of penetration, the rate of acceptance of, for example, assisted living or independent living is a key indicator in a marketplace area as to what the demand will be in that marketplace area. Another factor are the tradeoffs. And I’m going to talk more about penetration and acceptance, because I think in the U.S., I’m certain in the post Covid19 time, in the post Covid19 period, acceptance and penetration will be a key metric in determining how we emerge. There’s also a tradeoff between and among the risks and the utilities.

It’s a risk reward balance that’s now changed. Consumers are going to be much more sensitive to the potential risk associated with infection and illness than they have historically in these markets. Properties assisted living residences in particular, present, many of them present beautifully and offer some of them stunning interior environments.

When a consumer enters these environments, this curb appeal, this immediate sensory input pushes other factors to the background. Historically, it’s done. So, we need to be aware that going forward, those consumers who come to our doors will look first at our cleanliness and disinfection protocols and secondly at our chandeliers and the smell of freshly baked bread wafting through the lobby. These the utilities, the benefits and risks will be balanced and as has always been the case, the critical competitor to independent living, assisted living as a lifestyle choice, and this includes CCRC, is the status quo. What are people giving up? What are people gaining? And we all know that the loss of any benefit like health overwhelms the risk of losing another benefit like health.

These factors that benefit risk and the status quo will play a huge impact, have a huge impact going forward on how quickly assisted living in particular and independent living as well, and CCRC are once again accepted as a solution.

Furthermore, in those marketplace areas where there’s a very high acceptance and we know where those are, those are marketplace areas where there’s an assisted living residence on it, on every other block in those marketplace areas, that recovery will be swifter than in marketplace areas where lifestyle choices congregate. Seniors lifestyle choices are not as popular. The next factor that we need to look into or consider is the government and regulatory intervention, what government will do as the result of the tragedies unfolding in skilled nursing in particular, and assisted living residents as well. What governments are doing is nothing short of amazing.

You have on one hand a state issuing orders to nursing homes, telling them they have to accept patients from hospitals and the nursing homes, having no protocols for that, no personal protective equipment, no protocols for how to screen and properly screen. And then if someone screens out, what do you do with them? These types of things are playing out in the marketplace, in your marketplace, across the country to how the government response to this is going to be very interesting to watch and track. Finally, and I don’t want to get too deeply into the weeds, but insurance, liability protection and exposure risk management from an insurance perspective is also going to play an extraordinarily important role in this recovery. We’ve seen this already with OSHA just this week, issuing guidelines about employees functioning within skilled nursing centers. We’re going to see the insurance industry stepping up and attempting to understand and mitigate their risks because, of course, their risks in this regard are enormous.

The post Covid19 models, we already talked about the factors, these factors of acceptance, regulatory change, they’re going to affect the depth length and the shape of the recovery. And I’d like to propose that there are two scenarios in these three markets. The first scenario, it might be overly optimistic. Is that the sector will actually get rebuilt. That’s significant component, especially of the skilled nursing regulatory complex will be revised and that this will recharge those markets, the recovery in the sniff environment could force governments to look at the preparedness of skilled nursing centers for these kinds of challenges. The current situation could highlight the critical role that skilled nursing centers provided communities and may actually stem the raft of closures and bankruptcies that we’ve seen as the result of the decaying economic model in nursing centers. The recent spate of bankruptcies has been extremely burdensome, especially to rural and urban communities. So, we need something like a safety net nursing home model. Senator Kennedy in 2009 actually proposed a sweeping reform called a class act, which provided some of the funding and some of the structure which in this commentator’s opinion were needed to address some of these issues.

But that’s an scenario one where rebuilt and recharged. Scenario number two, unfortunately, is that we could be ravaged by death and relegated to permanent second-class status, especially in nursing homes. Remember, for the assisted living community, there will be knock on negative effects to what happens in nursing homes, consumers who aren’t able and families who aren’t able to secure proper skilled nursing placement for a consumer, for example, with neurodegenerative disorder who truly needs and want a secure skilled nursing placement, they’re going to wind up in some kind of assisted living. So that will create a whole set of knock-on effects in many marketplace areas.

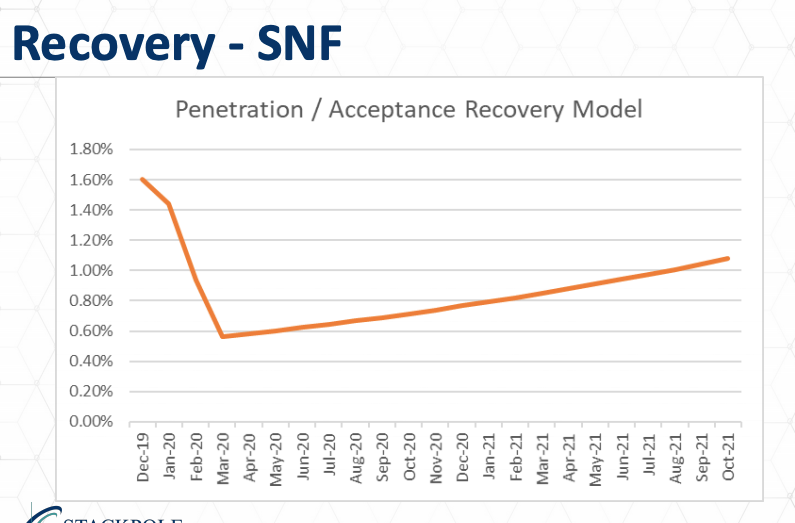

Let me let me go on to what I believe to be some three or four likely scenarios for recovery. In the sniff environment, what I’m suggesting is that we have gone very quickly from roughly 1.5 percent penetration and acceptance, that is to say, of the age qualified consumers in any given marketplace area, roughly 1.5 to 1.6 percent pre Covid19 were inside of skilled nursing centers. We’re going to see that, or we have seen it drop off. The front door is closed. Very, very few new consumers being admitted to skilled nursing centers, while there’s quite a few leaving for a variety of reasons. And this recovery will take quite a bit of time.

This model shows a recovery at a very gradual rate, looks more like an L. Shaped recovery, and all the way up to October in 2021, when GDP in the United States should be returning to baseline, we still see a depression or a negative effect on skilled nursing occupancy. Now this won’t be in every skilled nursing center, certain skilled nursing centers that are very progressive, that have very aggressive marketing communications programs, that have very aggressive outreach, significant community and referral source connections. They will fare better. But this is my best estimate, is how this sector on a national basis will recover. Assisted living residences are in a different position, may start in a different position. The national averages for acceptance or penetration is about 12 percent certain marketplace areas are much higher than that, and other marketplace areas are much lower than that. But the national average is about 12 percent. We see that going down precipitously already have seen it going down precipitously and then going through a gradual recovery.

It probably won’t be this smooth in certain marketplaces like Dallas, where we’re seeing recently a spike in some new infections and new hospitalizations that will cause this on the accelerator, on the brake, on the accelerator, on the brake sort of recovery in that marketplace area. But the overall assisted living residence, market demand penetration and acceptance will recur, will return, will recover, and it will recover more quickly than skilled nursing.

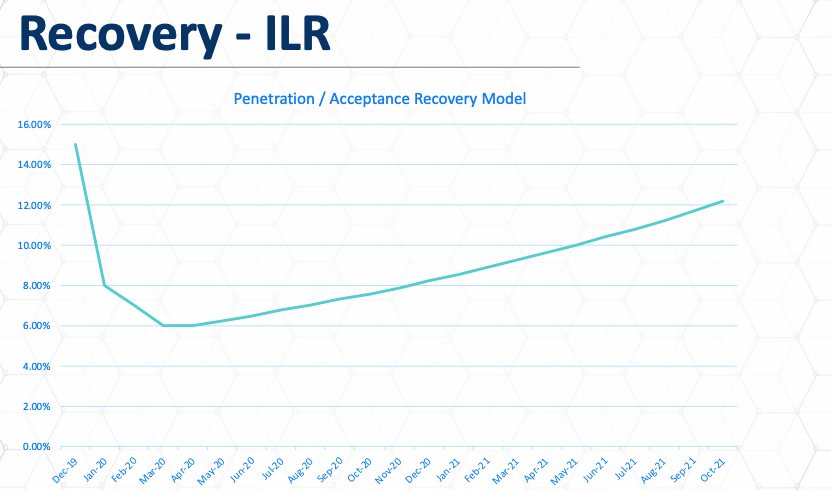

For independent living, the numbers of the current starting point for independent living are a little tougher to fix, but I’m guessing its around 15 percent based on several regional studies that we’ve done in certain marketplace areas. Again, it might be a little higher or a little lower, but we see a much faster return toward baseline in the post Covid19 period. Some reasons for this is branding. Independent living residences aren’t branded as health care solutions. They’re branded as social solutions. Not that I think that’s an option for assisted living residents. These properties also are savvier marketers. They do a better job with their digital assets. They do a better job reaching out to their marketplace areas and have deeper community networks in that regard.

So once again, that these are likely recovery models. There are certainly no guarantees. But the factors that we’ve already discussed in terms of penetration, in terms of the starting point in a particular marketplace, these will have a significant impact on the depth, length and the shape of these scenarios.

What can we do, what we are here in this tragic situation, congregate care is the perfect breeding ground for the coronavirus. It’s the transmission options are too many, too varied, too great. The specter not due to its own fault. In most cases, the sector was slow to respond because it didn’t have the PPE and because it got completely conflicted and mixed signals from the from its strategic and its regulators. So, what do we do? What’s next? I’m going to suggest there are two basically two options. One is that we can take the victim role and we can adopt you need to help us position or we can take on a change agency role. And while these two aren’t necessarily exclusive, mutually exclusive, it is important that you understand, I believe, in communicating and developing a position to recover from this pandemic in congregate Senior Housing and Care.

It’s important to understand who’s doing what and why and not only to determine what you’re going to do, but what others are doing as well. And here’s the first set of things that I believe it’s up to us to do. First is take responsibility for the messages. This was the focus of the crisis communications webinar I gave a couple of weeks ago. We know it is well known in the public relations and science, marketing, science communities. It’s well known how to manage communications in a crisis. It’s stunning to me how few nursing centers and an assisted living is a little better at it, but how few people actually employ those tools. They are ready and able to be used and they work. The last thing we should be doing is waiting for the media or special interest groups to drive the narrative or to shift the rhetoric toward shame or blame. Now, I do see in the media special interest and think tank policy development personnel, university-based think tanks pointing to the government’s inability to provide. The right tools, the personal protective equipment, disinfecting screening tools, protocols, the government’s inability to provide those, and yet at the same time, the government’s requirement that everybody be tested. Well, where are the tests? You can’t require somebody to test everybody if I’m a nursing home operator, if I can’t get the tests.

What’s critical is that we move and shift the narrative now. While there’s a still listening, while there’s still tolerance and acceptance of the messages, this is the time to start putting into the public spaces the messages about the value of what we’re doing and not just the hero’s work here message. That’s a very good message, don’t get me wrong. But the other message is about the role of the senior congregate care center in the community, what’s occurring, what has occurred inside the community, human interest stories, what the community can teach us about solidarity at a time of isolation, what the community can teach us about things like nutrition, what the community can teach us about things like caring for the mental health and wellbeing of the staff members who are caring for the most vulnerable members of our community. So, all of those messages can be associated with your brand and will be taken up in the markets in a very positive way and will counterbalance any of the negative messages, any of the shaming messages that come out of private special interest lobbying groups that want to. I don’t know what they want to do, but I see the messages in the media by groups who seem to want to put every nursing home out of business, shaming and blaming without seemingly without a purpose.

The other thing that we desperately need to do is we need to review our digital assets. Families are now using the Internet and social media channels more than ever. All the data is very clear. And this crisis, this pandemic has pulled us into the digital arena. Whatever can be done to improve the performance, enhance your digital assets. Crisis communications is critical. I believe that there are many organizations that are now offering crisis communications programs. I think we need to accept and understand the risk aversion, the fear that our consumers and our clients have now and will have for some time to come. I believe that this is not a permanent characteristic of the market dynamics in congregate senior’s care, but it’s certainly going to endure for the next eighteen to twenty-four months. So, we need to understand it and adapt to it effectively, both in our marketing messages and in our sales interactions.

One of the things I want to point out about fear and fear is the obverse, the opposite side of the coin of safety and safety is a must have quality. It’s the kind of quality that needs to be there in order for the consumer to notify the provider to be in the game, the consumer needs to feel safe. Well, now the consumer doesn’t feel safe and the consumer may not feel safe necessarily because of you and the solutions you’re offering, but because of the overall general environment. So how you address that is going to be going to be critical segmentation. We need to look at segmentation in the long-term care markets, as we have not done previously. There have been some segmentation studies done. We’ve done some of them, but there’s been far too few. We need to better understand the psychographic, not just the demographic or econometric, socio sociological, but we need to understand psychologically who chooses our solution and who doesn’t and why. That’s that’ll be an important piece. The segmentation needs to be done for SNF consumers and staff because staff is going to be the staff is the means of production in both SNF and Alar. And how we recruit and retain staff going forward will be critical to our ability to fulfill and recover effectively. Number four, in the current market, we need to defend, fortify and protect value. The value proposition we offer to our consumers is much more than a quid pro quo. It’s not transactional. The value derived by our consumers is it is far deeper than that. And we need to understand that. We need to understand that also about our staff. And we need very effective, rigorous service error recovery because in the post Covid19 environment, securing new market share, new prospects are going to become much more difficult, much more expensive, and the conversion rates will be lower.

So we need to be very effective at recovering when there is a service error. Finally, with regards to the future market, what we need to do is we need to innovate. Innovations up to this point have been very slow. We need deep seated innovations and the real shift in technology, why the sector hasn’t been pushing its technology providers even harder. We all need to be pushing the technology envelope to discover how we can improve efficiency in the post Covid19 period.

So I’ve tried to cover the current situation, likely recovery models with scenarios, some what I believe to be effective responses that we can undertake now and to review what it is that managers can do. Although I’m always at risk here, I can’t see your faces. The single biggest problem in communication is the illusion that it has taken place. Thank you, George Bernard Shaw. And with that, I would welcome the opportunity to respond to your questions.

QUESTIONS

QUESTION: So now let’s open the Q&A session. Why do you think the liability and protection of long-term care facilities change due to the new cleaning protocols?

Irving Stackpole Well, liability insurance, the risk-based model for protecting long term care centers is driven by, obviously, risk data. And I know because the insurance companies have been quite transparent in publishing their information about their risk modeling based on Covid19. I know that they’re still trying to sort it out and figure out exactly how to calculate risk models around infections in versus deaths in disability in long term care settings. I can’t say with any certainty how, but I am confident that the data is being scraped and collected by actuaries even as we speak and looked at very carefully. I would say categorically that your infection and disinfection protocols, I’m sure 86.4 percent of, you know, two standard deviations are excellent and some of them are really best in class. But world class disinfection and infection control protocols, we need to promulgate, promote and communicate about those in ways that we never have before because safety and cleanliness was assumed. Now we need to be far more forward in our communication about our infection control and disinfection protocols to the point where we could and should create symbols, plaques, models, stickers that show that this is this has been treated, this is disinfected. And there’s no you know; we’re all getting used to the fragrance of alcohol wipes in our physical environment.

QUESTION: What specific types of technology do see make an impact on long term care?

Irving Stackpole I’ve spoken about this for years and written about it extensively. Your local grocery, I’m going to be blunt, your local grocery store has more sophisticated technology than your nursing home. It should be a national embarrassment. Nursing homes, it’s the land that meaningful use left behind. We were nowhere at the table when the moneys were doled out to create affiliations, connections and interoperability of electronic health records. And why is that? That’s another conversation. We I would ask you this. So, what sort of technology can you track the location of your most expensive asset at any given point in time, on any given day, at any given moment, and in 99 percent of the nursing homes in the world? The answer to that is no. What’s your most expensive asset, your most expensive asset is your people, and I’m sorry for any people out there who are offended by my referring to them as means of production or by referring to them as assets, but as from an econometric point of view, that’s indeed what they are. And we have neglected that. 60 to 70 percent of your budget is people, and you don’t. I’m sorry, but we don’t know what they’re doing at any given moment in time. We have policies and procedures and guidelines, but we don’t really know. We need technology that allows us to track, analyzed and correct behavior in almost real time.

QUESTION: Do you see a decline in short term rehab admissions post Covid19

Irving Stackpole Oh, yeah, absolutely. It was already headed down. Medicare Advantage was our biggest that market’s biggest enemy, Medicare Advantage, saw a decline. But in many markets, pretty say in 2017-2018, we’d see 15, 18, 20 percent of the clean hips, knees, lower extremity. The proportion going to skilled nursing is going down. And the reason for that is that the data makes it clear and it’s a very good paper that was just published in Health Affairs I think last week. It shows that that the rehabilitation in the post-acute care rehabilitation did not make a significant difference in enough of the cases to warrant the expense.

Now, I push that back at the sector to say, why are we letting somebody else tell us what works? We have the data. Why aren’t we making the case right? Not everybody should come to skilled nursing for post, for post the doctor period of rehabilitation, but a certain group should. And here’s the evidence as to why and make the case from our data back to the intermediary as to why this should occur.

QUESTION: Given the huge financial cost to providers of responding to this crisis, do you think providers have enough left to invest in the program contains, as you are advocating?

Irving Stackpole No. What we what we know is from the good work in certain state societies and state organizations, the average daycare average days of cash on hand in many nursing centers in the United States was four to 10 days. For the four to 10 days. The burdensome, the burden of cost, direct, indirect and induced costs of this pandemic are significant. And they weigh very heavily on a system that was already creaking under an antiquated economic model that was that’s really preposterous and unsustainable. So, no, I don’t think the resources are there. If the associations, the thought leaders want to pick up any bit of shaming and blaming, it’s to get some of the billions of dollars that are getting thrown around to grab some of that for the express purpose of addressing these infrastructure issues in skilled nursing so that when the next crisis hits, not if, but when the next crisis hits, at least the surviving SARS have immediate and immediate no strings attached access to the tools and the resources that they need to mitigate death and illness.

I look forward to seeing you at the next webinar, thank you all and stay safe. Thank you.

Resources

- The Health Foundation

See: https://www.health.org.uk/publications/long-reads/health-and-social-care-workforce - This matrix from McKinsey shows the possible economic recoveries based on two factors

See: https://www.businessinsider.com/economic-outlook-9-scenarios-coronavirus-recovery-recession-mckinsey-experts-2020-4 - Congregate Long-Term Care: The Road to Recovery?

See: https://stackpoleassociates.com/seniors-housing-services/congregate-long-term-care-the-road-to-recovery

Stackpole & Associates is a marketing, research & strategy consulting firm focused on healthcare and seniors’ services markets. Irving can be reached directly at istackpole@stackpoleassociates.com.